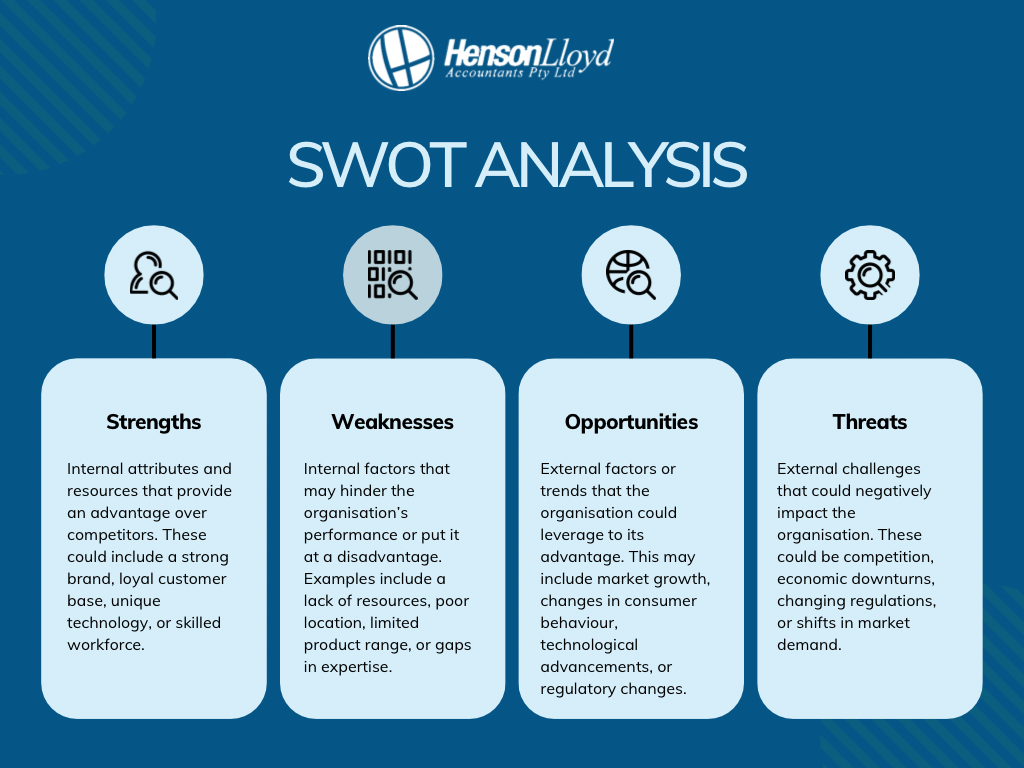

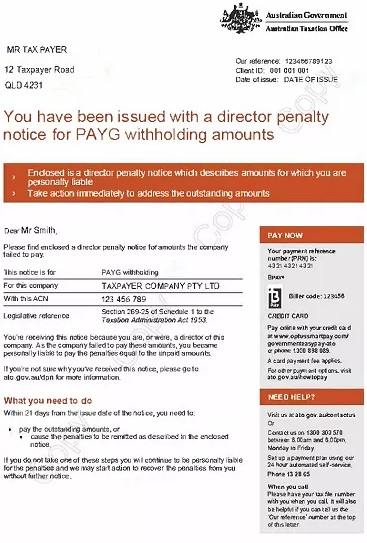

Newsletters We have a re-elected Labour Government & this is their housing platform. Read More → How Rework Reduces Your Profit – And What to Do About It Read More → Important Updates for Small Business Owners Read More → The Key to Success in Business is Embracing Change Read More → How a SWOT Analysis can help your business! Read More → Ensuring Compliance with Supplier Payment Obligations Read More → Surge in Director Penalty Notices: What You Need to Know Read More → Achieving Business Success with SMART Goals Read More → Claiming deductions in relation to a holiday home Read More → Sale of land subject to GST Read More → Changes in reporting requirements for sporting clubs Read More → Henson Lloyd Shines on National Television: AFL Sunday Show Feature Read More →